Preface

This article was written by Alexandre Thibault. An entrepreneur, lawyer, investor and strategic advisor, he also serves as the Chief Expert-in-Residence at DMZ’s tech ecosystem in Toronto.

At the bottom of this page, you can find the data that fueled this analysis of initial fundraising and seed rounds in both Quebec and Canada’s venture capital landscape.

This article was written by Alexandre Thibault. An entrepreneur, lawyer, investor and strategic advisor, he also serves as the Chief Expert-in-Residence at DMZ’s tech ecosystem in Toronto.

At the bottom of this page, you can find the data that fueled this analysis of initial fundraising and seed rounds in both Quebec and Canada’s venture capital landscape.

Startup funding: what should we expect?

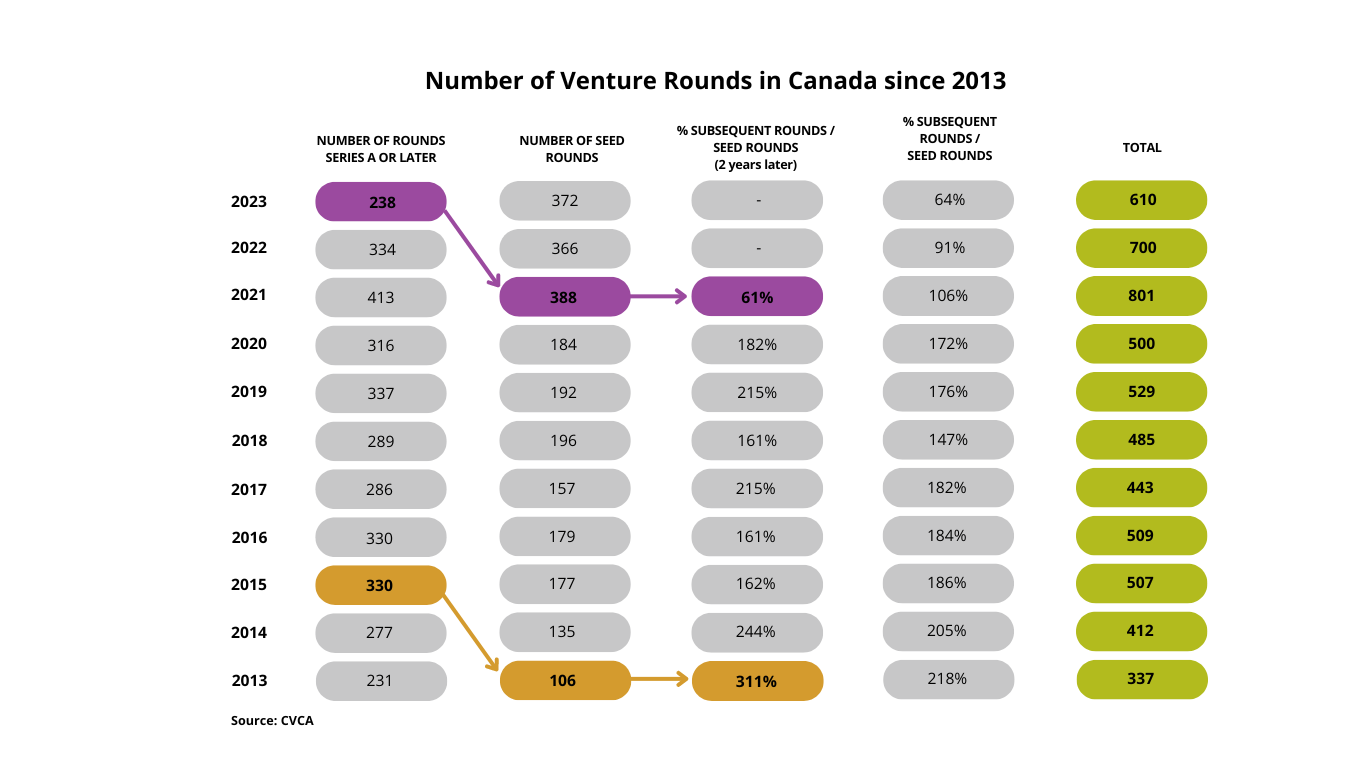

We recently came across the article “3 Charts: The US has more startups than VCs can support.” If you have not read it, the title says it all. In short, the market is dictating a new reality, compelling American startups to be more creative in their strategies going forward. But what about Quebec and the rest of Canada? Clearly, the end of zero interest-rate policy had a substantial impact on the landscape for tech startup funding here as well. On this side of the 49th parallel, much has been made about the 42% decrease in the number of Venture Rounds (Series A and beyond) between 2021 and 2023. Looking at this single statistic, one suspects that entrepreneurs should not rely as much on this funding to ensure their projects have enough gas in the tank. However, this picture does not tell the full story. To complete it, we pulled historical funding data since 2013 and pieced it together with Réseau Capital. See what we found:-

-

- Funded companies are more mature. The average age of a Canadian startup raising its first round rose to 3.65 years in 2023, the highest in the last 10 years and a 35% increase since 2014. Companies are waiting to be more mature, have more revenue and a better product-market fit to raise their first dollars.

-

-

-

- Larger rounds. As a direct consequence of the point above, entrepreneurs are able to get more capital in their initial fundraising. The median size of the first rounds involving a VC in Canada increased from $1 million in 2014 to $2.50 million in 2023. As recently as 2020, this amount was only $1.34 million before climbing abruptly.

-

-

-

- The number of seed rounds has nearly quadrupled in 10 years. Many have reported this, but market interest has shifted significantly towards seed rounds where the waters were calmer. This is quite encouraging for the longer term.

-

-

-

- Time between a startup’s first and second raise remains constant despite the turbulence. Since 2014, the average has been around 2 years plus or minus a few months. It was still the case in 2023, at 2.02 years.

-

-

-

- A steep drop in the ratio of Venture Rounds (Series A and beyond) over Seed Rounds. For every seed financing in 2013, there were 2.18 financings (218%) in Venture Rounds (see table below). This ratio was balanced in 2021 and declined in 2023 to reach 0.64 (64%). This is partly explained by the large number of Seed Rounds (see number 3 above), but not solely. The next observation rounds out this picture.

-

-

-

- Winter is coming. We know that a company seeks funding approximately 2 years after its previous raise (see number 4 above), so comparing numbers over three calendar years is the best way to make a prediction in this market. When we compare Seed Rounds to the number of Venture Rounds two years later (see purple and orange in the table), we see a 5X drop, from 311 % in 2013-2015 to 61% in 2021-2023. It is therefore much more difficult for a company looking for a Venture Round these days.

-

Ready to dive into the data that fueled Alex Thibault’s insights for his latest piece? Simply grab a copy of ‘Deciphering the initial VC fundraising rounds and seed rounds in Quebec’ from Réseau Capital’s Centre of Expertise. It’s your backstage pass to understanding the nitty-gritty of startup funding in the province!